Banyan’s equity composite gained 6.8% year-to-date through September versus 14.8% for the S&P 500. Since the start of 2019, when yours truly officially took the helm, we have compounded at 13.3% per year versus 17.5% for the S&P 500. Please refer to our equity composite for details.

This has been an interesting year. We outperformed the S&P 500 by more in Q1 than in any quarter since Q1 of 2013. Then, in Q3, we had our second worst quarter of underperformance in Banyan’s history. Only Q4 of 1999 was worse. That date should ring a bell. Coincidence? You decide . . .

Vices, Sins, & Flaws

“You don’t know a man if you can’t name his vice.”

- Southern Proverb

There is much truth in this proverb. I can name a vice or sin of every person I know well, and they can do the same for me. You can surely sympathize. We all have shortcomings. Even the Disciples were sinners. So, show me a man without a vice, and I’ll show you a man you do not know.

The same is true of businesses. They all have flaws, but flaws are easy to forget when business is good. This is where danger lurks. Fancy valuations follow flush profits and praise. So, too, does hubris. It is then that the seeds of failure are sown. Fancy valuations wilt once the weeds crop up.

The Big Five of AI – Microsoft, Meta, Alphabet, Amazon, and Nvidia – are a prime example. They have led the AI charge, which “accounted for pretty much all the S&P 500’s rise since the public launch of ChatGPT in late 2022,” says Barron’s.1 The Big Five now account for 25.6% of the S&P 500 as a result. But flush with profits and praise, are they now sowing the seeds of failure?

Absolutely not, says Wall Street. It says the Big Five will earn $846 billion in 2029.2 That exceeds 45% of Mexico’s economic output in 2024, and Mexico is no slouch. Its economy is the 12th largest in the world. Yet, $846 billion of profits amounts to less than 5.5% of the Big Five’s current market value. A 5.5% earnings yield is hardly generous, especially when it lies more than four years out.

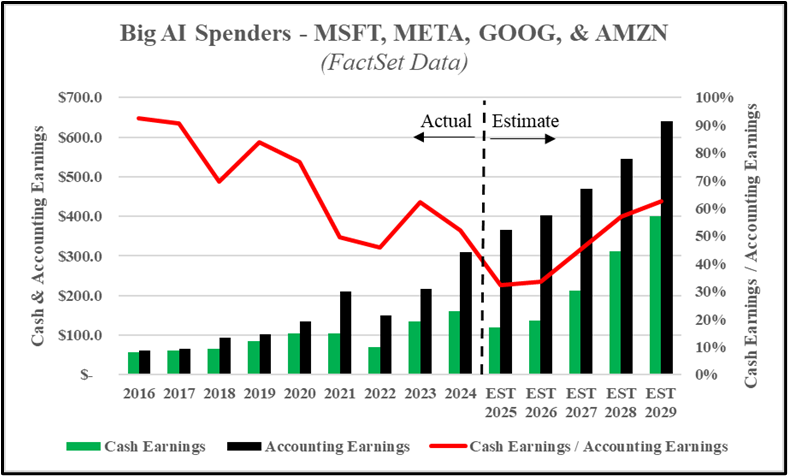

Moreover, those future profits assume a big payoff on a massive AI bet. Wall Street expects four of the Big Five – Microsoft, Meta, Alphabet, and Amazon – to spend over $2.1 trillion on CapEx between 2025 and 2029 (not a typo). The CapEx of these big spending titans nourishes the fifth, Nvidia, as they build the data centers in desperate need of Nvidia chips to handle AI workloads.

These four big spenders are some of the most profitable firms in history. Yet, the scale of this AI bet is straining even their finances. In 2025, for instance, their cash earnings (free cash flow less stock compensation) will amount to only 33% of their accounting earnings. Cash earnings were actually negative at Alphabet in Q2, which would have been unthinkable a few years ago.

It takes mighty flush profits and praise to bet the farm on a new technology, and betting the farm they are. “Over the past three years,” reports The Wall Street Journal, “leading tech firms have committed more toward AI data centers . . . than it cost to build the interstate highway system over four decades” in inflation-adjusted terms.3 A lot of profits are needed to nourish all this capital.

By 2029, for instance, these four big spending titans will have an additional $1.1 trillion employed in their businesses due to this CapEx boom. Thus, an extra $220 billion of profits must be squeezed from this new technology each year to get a mere 20% return on the capital employed by just four firms in five years on (mostly) one asset – data centers. That is a big number for even these titans.

Before 2024, in fact, these four big spending titans never collectively earned $220 billion in a year despite dominating wildly profitable businesses. It seems odd, then, for Wall Street to assume they will quickly squeeze $220 billion of profits from their AI investments while competing fiercely with one another. The economics would need to be extraordinary.

AI data centers are very capital-intensive, however, and they depreciate fast thanks to technological obsolescence. As a result, cumulative depreciation charges of $1.1 trillion and annual depreciation charges of $300 billion are expected for these four big spending titans by 2029. That is a daunting depreciation schedule, and it will make earning $220 billion of extra profits all the more difficult.

After crunching the numbers, Bain & Company thinks AI users must cough up $2 trillion for AI services each year to justify this level of investment.4 That is over five times the amount spent on global software subscriptions each year according to The Wall Street Journal.5 AI must therefore displace the entire software industry while not impairing monetization.

That seems unlikely. The data center (or “Cloud”) revenue growth at these four big spending titans has slowed, in fact, since AI emerged.6 Worse still, the price of AI services is already falling as AI models commoditize and competition heats up among Cloud providers selling compute capacity.7 But don’t take our word for it. Ask OpenAI’s ChatGPT. We did. Its response:

As prices fall, usage must grow even more dramatically to make up the difference. Yet, McKinsey says 42% of firms “abandon[ed] most of their [AI] pilot projects” in 2024 versus 17% in 2023.8 An MIT study shows why – 95% of firms using AI reported no financial payoff.9 Even software developers, who should benefit most from AI, saw their productivity fall 19% when they used AI.10

These are concerning omens. Hence the circular deals needed to keep the AI party going. OpenAI inked deals for $1 trillion worth of compute capacity in 2025 alone.11 Its revenues are $13 billion.12 To bridge the gap, OpenAI secured a $100 billion investment from Nvidia and 1¢ warrants for 10% of AMD’s shares.13 Nvidia and AMD are funding OpenAI’s purchase of their chips.

Perhaps this “whatever it takes to keep the party going” behavior explains Wall Street’s optimism. It profits off trading and capital raising. Activity, not wealth creation, serves Wall Street’s interests. It is Mr. Market’s hype man, not his chaperone. Mr. Market’s mood sets prices, in other words, and prices dictate expectations on Wall Street. Narratives emerge ex post to justify it all.

We, on the other hand, declined our invite to this party. AI may indeed change the world, but it is “not . . . how much an industry is going to affect society, or how much it will grow,” that matters, counseled Warren Buffett in 1999.14 Only profits matter, and profits may fall, not rise, for the Big Five as capital charges mount, malnourished capital decays, and this CapEx boom turns to bust.

The seeds of failure have been sown in our opinion, and markets are dreadfully exposed. Over one third of the S&P 500 is invested in the Big Five and three other AI darlings – Broadcom, Tesla, and Oracle. As shown below, cash earnings this year at these eight AI darlings will amount to only 1.1% of their combined market value of nearly $20 trillion (again, not a typo).

When the party gets out of hand, we must stand apart from the crowd to build permanent wealth. Q4 of 1999 was such a time. So is today. Your trust in us makes that possible. The opportunity cost is limited if we are wrong; a big AI payoff is already baked into the prices of these firms. If we are right, as we were in 1999, a spectacular hangover will be avoided. We welcome your questions.

Sincerely,

Drew Estes, CFA, JD

Portfolio Manager

See Other Resources

- Jack Hough, Trying to Ignore, from AI Polyamory to a Meme Fund Rebirth, Barron’s (Oct. 10, 2025), available at:https://www.barrons.com/articles/ai-warning-signs-stock-market-meme-convertible-bonds-ad0fbba7?st=BcxJNi.

- All Wall Street expectations cited here are median analyst estimates from FactSet.

- Eliot Brown and Robbie Whelan, Spending on AI Is at Epic Levels. Will It Ever Pay Off?, The Wall Street Journal (Sept. 25, 2025), available at:https://www.wsj.com/tech/ai/ai-bubble-building-spree-55ee6128.

- David Crawford, et. al., Technology Report 2025, Bain & Company, pp. 33, available at:https://www.bain.com/globalassets/noindex/2025/bain_report_technology_report_2025.pdf.

- Brown, Spending on AI Is at Epic Levels. Will It Ever Pay Off?, The Wall Street Journal.

- Cloud revenue growth rates have deteriorated at MSFT, GOOG, and AMZN since 2021 despite ChatGPT’s release in 2022. Their average revenue growth rate was 36.3% from 2020 through 2022 versus 22.7% from 2023 through 2025.

- See, e.g., Joe Green, The OpenAI Price Cut is A Dangerous Gamble, TechHQ (June 24, 2025), available at: https://techhq.com/news/the-openaiprice-cut-is-a-dangerous-gamble/.

- Steve Lohr, Companies Are Pouring Billions Into A.I. It Has Yet to Pay Off., New York Times (Aug. 13, 2025), available at:https://www.nytimes.com/2025/08/13/business/ai-business-payoff-lags.html.

- Sheryl Estrada, MIT Report: 95% of Generative AI Pilots at Companies are Failing, Fortune (Aug. 18, 2025), available at:https://finance.yahoo.com/news/mit-report-95-generative-ai-105412686.html (citing The GenAI Divide: State of AI in Business 2025 by Massachusetts Institute of Technology).

- Joel Becker, Measuring the Impact of Early-2025 AI on Experienced Open-Source Developer Productivity, Model Evaluation & ThreatResearch (July 2025), available at: https://metr.org/blog/2025-07-10-early-2025-ai-experienced-os-dev-study/.

- See, e.g., Eimly Forgash and Agnee Ghosh, OpenAI, Nvidia Fule $1 Trillion AI Market With Web of Circular Deals, Bloomberg (Oct. 7, 2025),available at: https://www.bloomberg.com/news/features/2025-10-07/openai-s-nvidia-amd-deals-boost-1-trillion-ai-boom-with-circular-deals.

- Brown, Spending on AI Is at Epic Levels. Will It Ever Pay Off?, The Wall Street Journal.

- Tabby Kinder and George Hammond, OpenAI’s Computing Deals Top $1tn, Financial Times (Oct. 7, 2025), available at:https://www.ft.com/content/5f6f78af-aed9-43a5-8e31-2df7851ceb67.

- Warren Buffett, Mr. Buffett on the Stock Market, Fortune (Nov. 22, 1999), available at:https://www.berkshirehathaway.com/1999ar/FortuneMagazine.pdf.

Important Notice

You are now leaving the Banyan Capital Management website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) website.

Schwab is a registered broker-dealer, and is not affiliated with Banyan Capital Management or any advisor(s) whose name(s) appear(s) on this website. Banyan Capital Management is/are independently owned and operated. Schwab neither endorses nor recommends Banyan Capital Management, unless you have been referred to us through the Schwab Advisor Network®. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Banyan Capital Management under which Schwab provides Banyan Capital Management with services related to your account. Schwab does not review the Banyan Capital Management website(s), and makes no representation regarding information contained in the Banyan Capital Management website, which should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

Continue to Website.svg)