Dear Client,

Banyan’s equity composite lost 2.2% in the first quarter versus the S&P 500’s loss of 4.3%. Since the start of 2019, when yours truly officially took the helm, we have compounded at 12.5% per year versus 15.9% for the S&P 500. Details on our equity composite can be found here.

Software Stocks

What happens when a coveted firm is suddenly loathed by investors? Nothing good, at least for its stock. The gap between “priced for perfection” and “priced for disruption” is large indeed. Glance at any software stock for proof. Many have fallen 40-60% in the past year. Sensing an opportunity, we bought three in Q1 – FactSet (FDS), Roper (ROP), and Wolters Kluwer (WKL in Amsterdam). We have long admired these firms. Until now, however, we were never tempted to buy them.

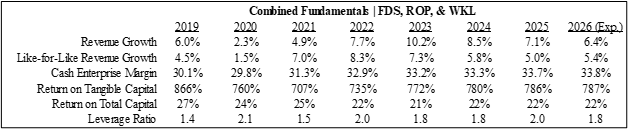

Quality was never the issue. All three are fantastic businesses. As shown below, their like-for-like revenue (i.e., excluding acquisitions, divestitures, and currency moves) grew by 6.3% per year on average from 2019 through 2025 ignoring a pandemic blip in 2020. Their pricing power was also evident with customer retention above 90% per year and over 95% for many products. They need almost no capital to operate and have enviable margins. There was little not to like.

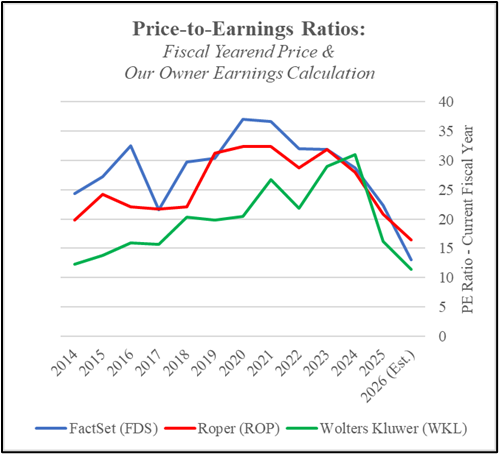

Unless, of course, you like good prices. Software stocks were market darlings, and they did what market darlings do – trade at fancy prices. As a group, the three we own rarely traded for less than 30x earnings between 2019 and 2024 (see graph below). It got our attention, then, when their prices fell below 20x earnings in late 2025. We still didn’t buy, though. Our taste is for less fancy prices, and that is what we got early this year. We could no longer resist at prices of 11-16x earnings.

“But,” you might retort, “the world changed with the emergence of AI!” Yes, of course it has, we can readily admit. AI’s emergence is material, and it has a clear nexus with software. Even we can code now, which says a lot, and we use AI almost daily in our studies. In that sense, we agree with our proverbial friend, Mr. Market. Software’s future is less certain. Accordingly, software firms no longer deserve such fancy prices (although we never thought they did).

We therefore have no quibble with Mr. Market paying less for these stocks. Our quibble is how much less he is paying. Mr. Market was certain these firms would dominate growing niches for decades when he paid 30x earnings. To now sell the same firm at 11x earnings, as is the case for WKL, he must now be just as certain of a bleak future. This certainty is what baffles us. We weren’t so sure of their multi-decade dominance before, and we aren’t so sure of their bleak future now. Hence our prior hesitation and present eagerness. At the prices we paid, these investments could be profitable so long as the firms don’t shrink; they may be a windfall if the outcome is better.

We like our odds. These firms should grow despite AI. None of the firms we bought have seen a change in their customer retention rates. This suggests their pricing power remains largely, if not entirely, intact. It is worth exploring why. They have many demand-side advantages:

- Switching Costs | People become habituated to software embedded in their workflow. This is true of individuals, departments, firms, and even industries as a whole. Once embedded, people’s work adapts to the software’s functionality, and switching is a very disruptive and costly endeavor. People on the frontlines inevitably fight it.

- Search Costs | A new software’s functionality cannot be fully assessed before switching. It must be used in one’s daily work to find its shortcomings, as anyone who has made a switch can attest. This advantages incumbents. Users know their existing software works well enough. A new solution must be compelling enough to warrant a risky leap of faith.

- Switching Risks | The leap of faith is especially risky for “system of record” software, and this is particularly so in regulated niches like banking and healthcare. The software contains user data going back decades in many cases. Data loss or corruption may occur in a switch. This can be an unacceptable risk that threatens a business user’s survival. It is worth noting, moreover, that AI is not well-suited for “system of record” uses. “Systems of record” turn user data into very specific outputs like regulatory reports. Users demand 100% accuracy 100% of the time. Software is great at this since its output is rules-based (or “deterministic”). AI is not. Its output is “probabilistic.”

These advantages give incumbents a lot of pricing power over existing users. We, for instance, use a “system of record” software for reporting that has hardly changed since the 1990s. They increase our price 6% per year. Superior products exist, and we have tried switching. It was a costly lesson. The other products’ shortcomings were not revealed until we used them in our work. We kept the old software after wasting a lot of time and money. What do they say about the devil you know?

Turning to the supply-side, software has two more advantages worth mentioning:

- Network Effects | Some software is a two-sided platform that grows more valuable as the user base grows. ROP owns DAT, for example. It is a freight brokerage platform. Shippers post loads on it, and truckers bid on the loads. Since more truckers use DAT, shippers get more competitive bids. That leads to better freight prices, which attract more shippers, and more loads then attract more truckers. DAT’s value is the network, not the software.

- Niche Knowledge | Niche (or “vertical”) software firms gather a lot of knowledge about a very specific workflow. They know what the workflow demands, what functions are most valued, and how each function interacts with others. New entrants lack this knowledge. As a result, their products tend to lack some critical functionality. When a new entrant manages to offer a valuable new function, however, incumbents can quickly replicate it.

That final point is worth reiterating. Adaptability is the defining attribute of software. Its stickiness and malleability give incumbents the luxury of being “fast followers,” which brings us to our most contrarian thought. If an AI function is valuable to users of a software product, then that AI function can easily be incorporated into the software. Most AI functions, after all, are ultimately derived from a few foundational models like Claude and ChatGPT. These models are available to all, cheap to use, and commoditizing quickly. Software may end up being the biggest AI beneficiary.

There is a final point to make. Firms like OpenAI are raising tons of money to cover their massive losses. This is a huge subsidy for AI users, and it is overstating AI’s value proposition. When prices reflect the true cost of building and running AI models, the universe of software threatened by AI will shrink dramatically. Why, for instance, would you pay an error prone AI agent to do your taxes when existing software can do it faster, with fewer mistakes, and at a lower price?

In short, software stocks may be the best opportunity we have seen. Yes, AI has rendered the future less certain, but, at the right price, uncertainty and building permanent wealth go hand-in-hand. That is the case here. We did, however, diversify our investment across three firms because of the uncertainty, and two of the firms we own (WKL and ROP) are themselves diversified. In addition, ROP benefits from lower prices as a serial acquirer. We look forward to watching them adapt.

Sincerely,

Drew Estes, CFA, JD

Portfolio Manager

See Other Resources

Important Notice

You are now leaving the Banyan Capital Management website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) website.

Schwab is a registered broker-dealer, and is not affiliated with Banyan Capital Management or any advisor(s) whose name(s) appear(s) on this website. Banyan Capital Management is/are independently owned and operated. Schwab neither endorses nor recommends Banyan Capital Management, unless you have been referred to us through the Schwab Advisor Network®. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Banyan Capital Management under which Schwab provides Banyan Capital Management with services related to your account. Schwab does not review the Banyan Capital Management website(s), and makes no representation regarding information contained in the Banyan Capital Management website, which should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

Continue to Website.svg)