Banyan’s equity composite gained 0.7% through the second quarter versus the S&P 500’s gain of 10.2%. Since the start of 2019, when yours truly officially took the helm, we have compounded at 12.5% per year versus 17.6% for the S&P 500. Details on our equity composite can be found here.

A Tale of Two Markets

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity . . . .”

- A Tale of Two Cities

Charles Dickens’ classic, A Tale of Two Cities, has one of the finest openings in all of literature. A juxtaposition hooks readers from the start, but the line is more than literary flair. It is also an apt description of the novel’s setting. The French Revolution was energized by liberal values much like the American Revolution, but it devolved into a murderous campaign against dissent. A revolt against oppression ended in more oppression.1 The novel’s opening line reflects this irony.

A novel set in today’s financial world could open with the same line. A similar title – A Tale of Two Markets – would also be fitting. Elon Musk would be the protagonist. Irony, after all, is his calling card. “[R]eality is an irony maximizer,” says Elon, so “the most ironic outcome is the most likely.”2 It is an interesting view. An event is ironic if it differs drastically from expectations. The greater the difference, the greater the irony. Elon may be onto something.

Irony, in fact, is at the heart of Austrian Business Cycle Theory. Entrepreneurs overinvest because they overestimate future demand. Their optimism about the future causes an economic boom in the present, but, ironically, what follows is a bust rather than bliss. Too much investment today produces too much output tomorrow. A painful liquidation of excess capacity is needed. The origin of the error is access to unnaturally cheap capital, which asset bubbles provide like nothing else.3

Perhaps the Austrian theory should be renamed. Elon’s Irony Maximizing Theory would get more attention, and it could hardly be more relevant. We are in the midst of an unprecedented investment boom in anticipation of future demand for AI. Consider the following data points:

- Just five firms are expected to earn $805 billion per year by 2029 after investing $4 trillion on mostly one asset – data centers for AI – over a mere five years (2025-2029).4

- Just eight firms selling inputs for AI data centers are expected to earn $848 billion in 2029 alone versus the $197 billion they earned three years into the investment boom in 2025.5

- These 13 firms, all among the 25 largest in the S&P 500, are therefore expected to earn 6% more in 2029 than all of the 487 other firms in the S&P 500 earned collectively in 2025.6

- Using these 13 firms’ 2025 net margins, which averaged an abnormally high 26.5%, $6.33 trillion of revenue is needed per year by 2029 for them to earn what Wall Street expects.7

- Despite the insanity of these numbers, investors are so sure AI revenue and earnings will materialize that these 13 firms trade today at 14.2x their expected earnings in 2029.8

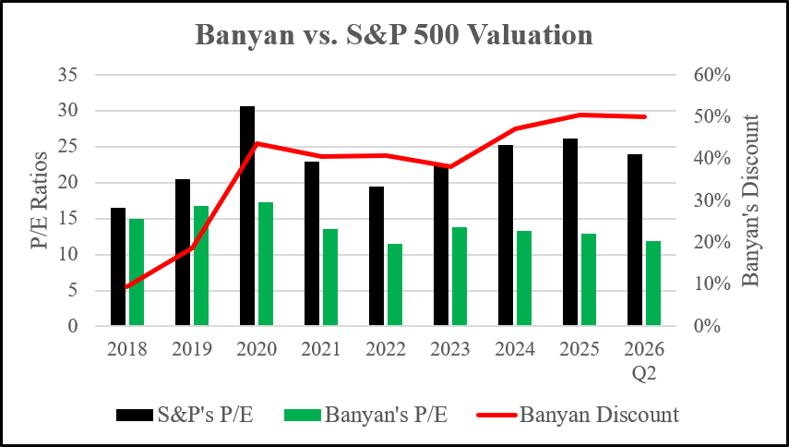

No wonder the S&P 500 is up so nicely. Since late 2022, when ChatGPT’s launch sparked the AI investment boom, a mere 28 AI-oriented firms are responsible for 63% of the S&P 500’s earnings growth and 76% of its price return.9 Earnings always boom, by the way, in an investment boom. The story is quite different for the rest of the market. Banyan’s portfolio, for instance, has not been this cheap since at least 2017 (see below). We also think our portfolio’s quality is at its highest.

A Tale of Two Markets indeed, but we could hardly be more optimistic. The divergence has allowed us to buy great firms at very cheap prices. We expect to reap the rewards in the years ahead. Our optimism does not, however, extend to the market itself. Its story is all about AI, and that story will likely end with an ironic twist. Such stories appeal to many; they are exciting. We, on the other hand, prefer boring stories. Building permanent wealth demands a more predictable ending.

Sincerely,

Drew Estes, CFA, JD

Portfolio Manager

See Other Resources

- We thank our friend Henry Oliner of Macon, Georgia, for educating us on the French Revolution.

- Elon Musk (Guest), The Joe Rogan Experience, Episode 2281 (Feb.28, 2025), Timestamp 2:20:58, transcript available at: https://podcasts.happyscribe.com/the-joe-rogan-experience/2281-elon-musk.

- See, e.g., Stefan Oppers, The Austrian Theory of Business Cycles: Old Lessons for Modern Economic Policy?, IMF Working Paper (Jan. 2002), available at: https://www.imf.org/-/media/websites/imf/imported-full-text-pdf/external/pubs/ft/wp/2002/_wp0202.pdf.

- Wall Street estimates, according to FactSet, for META, MSFT, GOOG, ORCL, and AMZN.

- Wall Street estimates, according to FactSet, for NVDA, AVGO, MU, AMD, INTC, CSCO, LRCX, and AMAT.

- FactSet data for 2025 earnings for all companies in the S&P 500 as of Q2 2026 excluding the above mentioned.

- FactSet data for 2025 earnings and revenue. Rounding is responsible for difference in calculation.

- Using recent market capitalizations and Wall Street estimates for 2029 earnings according to FactSet.

- Michael Cambalest, Smothering Heights, J.P. Morgan (Jan. 1, 2026), available at: https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/eye-on-the-market/smothering-heights-amv.pdf.

Important Notice

You are now leaving the Banyan Capital Management website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) website.

Schwab is a registered broker-dealer, and is not affiliated with Banyan Capital Management or any advisor(s) whose name(s) appear(s) on this website. Banyan Capital Management is/are independently owned and operated. Schwab neither endorses nor recommends Banyan Capital Management, unless you have been referred to us through the Schwab Advisor Network®. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Banyan Capital Management under which Schwab provides Banyan Capital Management with services related to your account. Schwab does not review the Banyan Capital Management website(s), and makes no representation regarding information contained in the Banyan Capital Management website, which should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.

Continue to Website.svg)